Lease Buyout Risk in 2026: How to Price the Residual and Check the VIN Before You Buy Your Own Car

A lease buyout can be a genuinely good used-car deal. Sometimes it is the easiest answer on the board. You know how the car was driven, you know whether it smells weird after rain, and you already know if the seat bothers your back. That is real value.

The trap is familiarity. People get so comfortable with "their" car that they stop evaluating it like inventory. They focus on the monthly payment they already understand and stop checking the same things they would check on any other used car: the VIN history, the recall status, the real market value, the tire and brake bill that is about to land, and whether the buyout math still works once taxes and fees show up.

This is different from our private-seller lien-payoff article and our used-car pricing post. Those deal with stranger-owned cars and broader market pricing. This one is about the false sense of safety that comes from knowing the car personally. A lease buyout feels low-risk because the vehicle is familiar. It can still be overpriced, overdue for maintenance, or awkward to finance if you do not slow down and price it like a used car.

Why lease buyouts fool smart buyers

Residual price

Feels fixed

The number is printed in the lease, so people treat it like the car's true value. It is not. It is just the contract number you need to test against the current market.

Known history

Feels safer

You know what happened in your ownership, but a future lender, insurer, or buyer will still judge the car through the VIN file and condition report.

Lease-end stress

Pushes shortcuts

Mileage charges, wear fees, and looming turn-in deadlines make a buyout feel emotionally urgent even when the math is only mediocre.

That is why lease buyouts deserve the same discipline as any used-car purchase. Maybe more. You are not just deciding whether you like the car. You already know you like the car. You are deciding whether this specific car, at this specific price, still makes sense in the used market right now.

The three numbers that actually decide the deal

-

Your real buyout total.

That means the residual plus purchase-option fee, sales tax, title and registration costs, and any dealer processing charge if the lessor forces you through a store. The residual alone is not the final number.

-

The current market value of similar cars.

Check current listings and trade-in guidance for the same year, trim, mileage, and condition. If your buyout total is higher than what comparable cars cost on the open market, the "easy" option may actually be the expensive one.

-

The catch-up money you will spend right away.

Tires, brakes, a recall visit, paintless dent repair, service you postponed because you were about to turn the car in, or a warranty gap you now have to absorb. A lease buyout can get ugly fast when the car needs $2,000 to $3,000 right after the paperwork clears.

This is the whole game. If the buyout total is competitive, the condition is solid, and the near-term repair bill is normal, buying your lease can be the calmest used-car purchase you ever make. If one of those numbers is off, the deal gets worse fast.

What people skip because the car already feels familiar

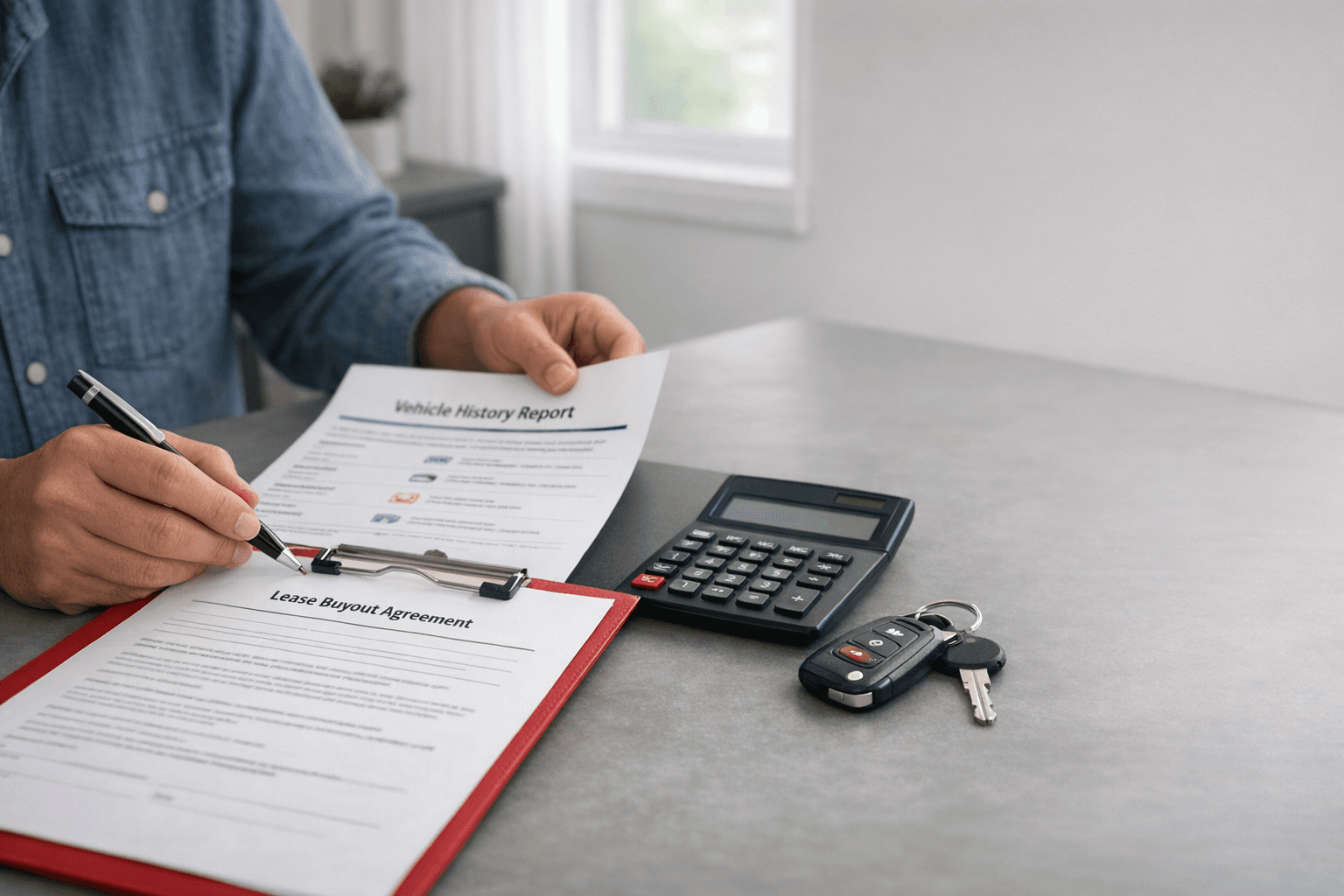

- The VIN history report. You may know the car never flooded or got stolen, but you still want a clean title, loss, and mileage file before you finance or keep it long-term.

- Open recalls. NHTSA still wants you to check recall status by VIN. Your memory of dealer visits is not the same thing as verifying the current record.

- A real condition check. Lease cars hit a weird stage near the end where owners defer maintenance because turn-in is close. Then they decide to buy the car and inherit the delayed bill.

- Future resale optics. The next buyer does not care that you loved the car. They care about title history, accident history, remaining warranty, tires, and whether the price is still defendable.

That future-resale point matters more than people think. I know it sounds odd to talk about your eventual exit before you buy your own car, but that is exactly the mindset that keeps lease-buyout math honest.

A practical lease-buyout checklist

-

Request the exact buyout quote in writing.

Get the good-through date and every fee. If the lessor or dealer will not give you a clean number, do not pretend the math is clear.

-

Run the VIN history report before you commit.

Treat your own lease like any other used car. Verify title status, mileage chronology, loss signals, theft records, and recall context.

-

Check open recalls by VIN.

If the car has an unresolved safety recall, clear that before you start rationalizing the buyout.

-

Price the car against current comps, not against your monthly payment.

People anchor on what they have been paying. That is normal. It is also how you talk yourself into overpaying for a used car you already recognize.

-

Inspect tires, brakes, glass, and deferred service honestly.

This is where the end-of-lease psychology sneaks in. If you skipped maintenance because you thought the car was going back, add that cost back into the deal now.

-

If you need financing, ask the lender how they will value the car.

A buyout that looks fine on your spreadsheet can still become awkward if the lender's advance or loan-to-value limit comes in lower than expected.

Proceed, negotiate harder, or let it go

Proceed

The buyout total is competitive, the VIN report is clean, recalls are handled, and the car does not need an immediate catch-up round of expensive work.

Negotiate harder

You still want the car, but the fees are padded, the tire or brake bill is real, or the market shows better pricing than the lessor is asking.

Let it go

The buyout total overshoots the market, financing is weak, or the car needs enough immediate work that the "easy" option stops being the smart one.

That last bucket is the one people resist because it feels like giving up something familiar. But a familiar bad deal is still a bad deal. Sometimes the best move is to hand the keys back and shop with a cleaner head.

Why VINSCRIBE matters on a lease buyout

VINSCRIBE helps you break the emotional spell of "but I already know this car."

- Run the VIN and verify the title, loss, theft, mileage, and recall story before you finance the buyout or keep the car long-term.

- Use one clean report when you compare market pricing, talk to a lender, or decide whether the car is worth another few years of ownership.

- Keep the decision grounded in the car's record, not just your memory of owning it.

That is the real edge. A lease buyout should feel easy because the car is familiar, not because you skipped the checks. Run the report from the vehicle history workflow before you sign anything new.