Used Car Dealer Fees in 2026: How Add-Ons and Payment Packing Turn a Fair Price Into a Bad Deal

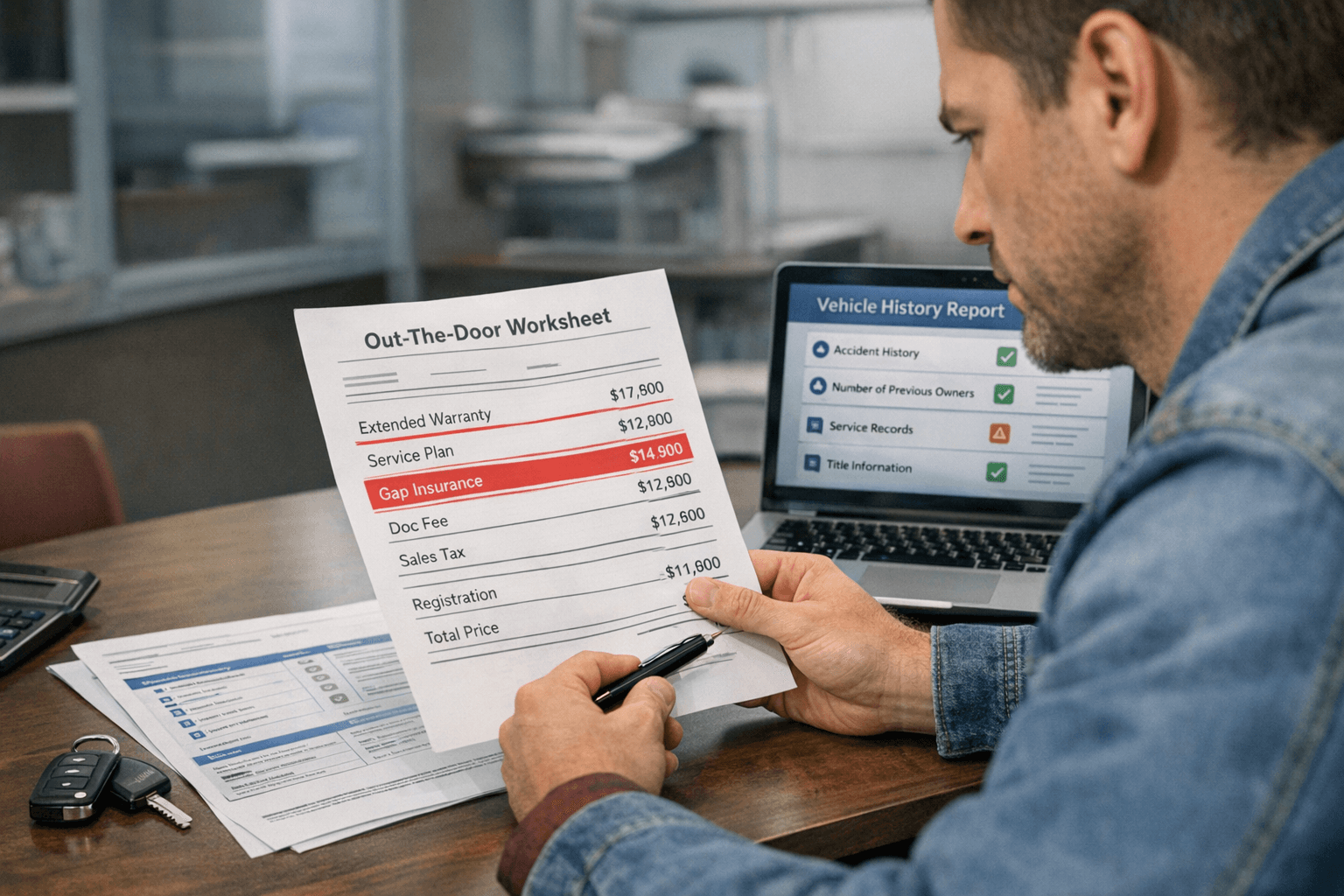

A used car can feel affordable right up until the moment the worksheet shows up. The online price looked fine. The test drive was fine. Then somebody prints the deal and suddenly you are staring at a doc fee, a reconditioning charge, window etching, a protection package, and a monthly payment that somehow matters more than the car's actual price.

This is where a lot of buyers get cooked. Not because they cannot do math, but because the deal gets reframed on purpose. Instead of asking, "What am I paying for this car?" the conversation turns into "Can you live with this payment?" That shift is where thousands of dollars disappear.

This post is different from our GAP, extended warranty, or yo-yo financing articles. Those cover specific finance products or financing traps. This one is about the broader fee creep that turns a decent used-car price into a bloated out-the-door number, especially when the car's history already gives you a reason to be skeptical.

Why this deserves its own used-car risk check

Listing price

Gets the click

It tells you almost nothing about the final number if the store loads the back end of the deal.

Finance office

Changes the frame

The conversation often shifts from total price to monthly payment because payment is easier to hide things inside.

Buyer mistake

Arguing one line at a time

If you only fight the extras after the credit pull and test drive, you are negotiating from a tired position.

I would not walk into a used-car negotiation without one hard rule: get the out-the-door price in writing before you discuss trade, down payment, or monthly payment. If the store will not do that, you already learned something useful.

Which charges are normal, and which ones deserve a hard look

Not every extra line is a scam. Some charges are real. The problem is that dealers often mix legitimate costs, inflated dealer fees, and optional products into one messy stack and count on you not separating them.

Usually legitimate

- Sales tax and state registration charges

- Title and plate fees

- A disclosed documentation fee, if your state allows it

Where I slow down

- Reconditioning, prep, inspection, or certification fees added after the advertised price

- VIN etching, nitrogen, wheel locks, GPS trackers, paint or fabric products

- Service contracts, GAP, key replacement, or maintenance plans presented like they are mandatory

The tell is usually simple. If a fee sounds like normal dealership overhead, I assume it should have been baked into the asking price already. If a product is optional, I want it itemized separately with a clear yes or no decision from me.

How payment packing hides the real overcharge

Payment packing is not magic. It is just psychology plus term length. Instead of saying, "You are financing another $2,400 in extras," the pitch becomes, "It only changes the payment by $38 a month." That sounds manageable because the loan term is doing the hiding.

-

The dealer starts with the monthly payment.

This keeps your attention on comfort, not total cost.

-

Optional products get blended into the financed amount.

By then the extras feel small because they are spread across 60 or 72 months.

-

The car itself stops being the central question.

That is how buyers end up financing backend products on a used car they have not even pressure-tested properly.

I do not think this is a small distinction. If the deal only works when the store keeps you focused on payment instead of price, the deal probably does not work.

Why vehicle history should change your tolerance for every extra fee

This is where VINSCRIBE matters. A buyer might grudgingly accept a few hundred dollars of nonsense on a genuinely clean, correctly priced car. That same buyer should have a very different reaction if the report shows accident history, auction movement, prior commercial use, a title issue, or a total-loss story that weakens the car's value.

Clean history

You are still negotiating price discipline, but at least the car starts from a stronger footing.

Messy history

Every add-on hurts more because you may already be paying too much for the vehicle itself.

Best leverage

Use the report first, then negotiate from the actual car story instead of from the dealer's menu.

That is the practical mistake I see most often. Buyers argue over nitrogen tires while ignoring the fact that the car itself may already deserve a discount because its history is weaker than the listing made it sound.

The questions worth asking before you let the deal move forward

-

What is the full out-the-door price right now, in writing?

Not an estimate. Not a worksheet that changes when financing changes. The actual number before you leave the store.

-

Which items are government fees, and which items are dealer charges?

Those are not the same thing, and they should not be blurred together.

-

Which products are optional?

If it is optional, I want to see the price and decline it cleanly if I do not want it.

-

What does the payment look like with every optional product removed?

That one question forces the deal back into the open.

-

What does the vehicle history report say before we argue about protection products?

If the VIN story is weak, there is no reason to finance more stuff on top of it.

A serious dealership can answer those questions without turning theatrical. If the room gets weird the moment you ask for clarity, that is not an accident.

Proceed, push back, or walk away

Proceed

The store separates taxes, state fees, doc fee, and optional products clearly, and the car's history supports the price.

Push back

The extras are removable, the vehicle checks out, and you are only dealing with a few padded lines that can be negotiated out.

Walk away

The store will not provide a clean buyer's order, keeps returning to monthly payment, or wants full retail money plus add-ons on a car with a questionable history.

I would add one more walk-away trigger: "every car gets this package." Fine. Every buyer can also leave.

Worth watching before you sit down in the finance office

These FTC videos are short and actually useful. One explains how add-ons get framed. One helps reset the financing conversation. The last one is a good reminder that advertised price and real deal price are often two different things.

What this means for VINSCRIBE users

VINSCRIBE helps buyers do the important part first: verify the car before they get cornered into defending the payment.

- Run the vehicle history report before you negotiate the finance-office menu.

- Use the report to push back if the dealer wants clean-history money on a car with accident, title, commercial-use, or auction baggage.

- Keep the car decision separate from the add-on decision. You can always shop a service contract later. You cannot unbuy the wrong car.

That is the cleanest way to think about it. First decide whether the car itself deserves your money. Then decide whether any extra product deserves more of it.

Start from the vehicle history page before you let the pricing conversation drift into monthly-payment theater.