Yo-Yo Financing Used Car Risk in 2026: How Spot-Delivery Deals Turn After-the-Fact Approval Into a Real Problem

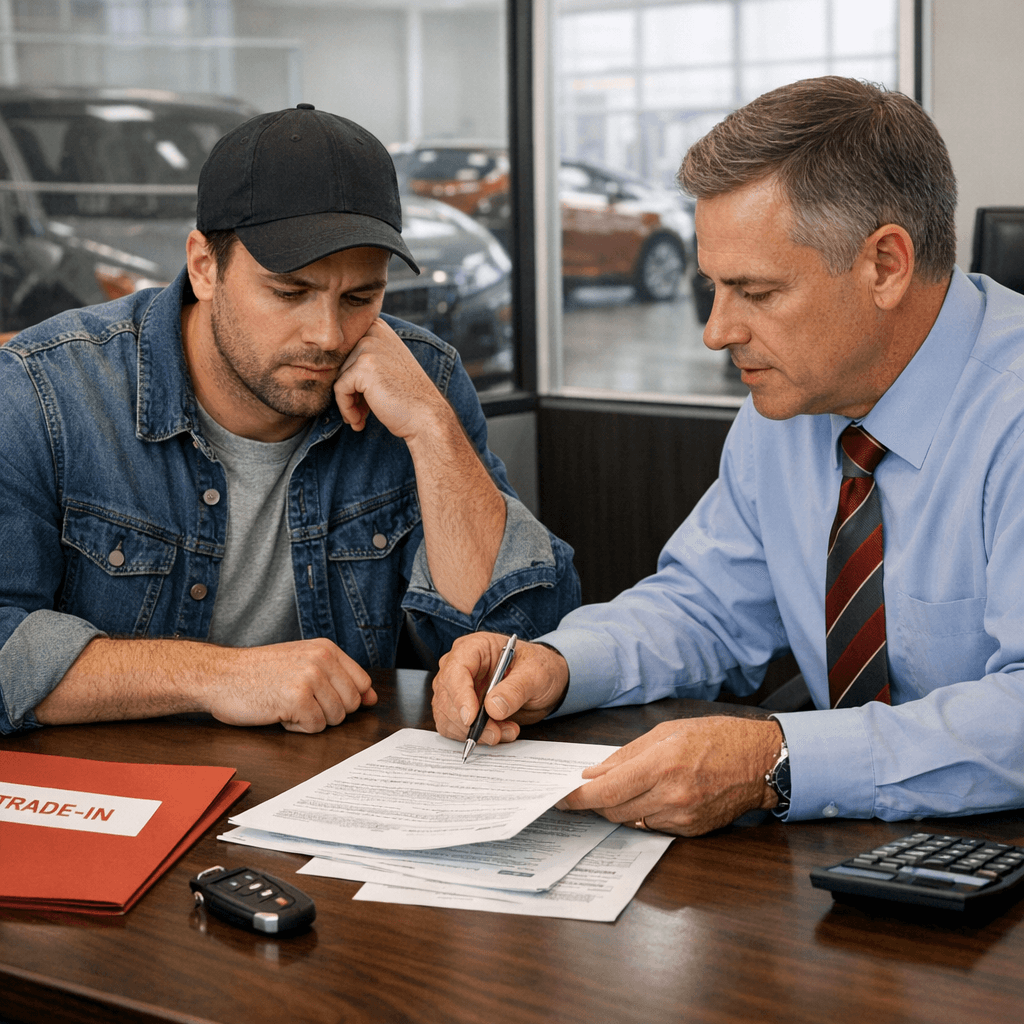

A lot of bad used-car deals do not feel bad on day one. They feel exciting. You pick the car, sign a stack of papers, hand over the down payment, maybe hand over your trade, and drive home thinking the hard part is finished.

Then the phone rings. The dealer says financing was not approved after all. They want you back in the office to sign a new contract with a higher rate, a larger down payment, or a steeper monthly payment. That is the basic shape of yo-yo financing, and it works because most buyers are already emotionally committed by the time the terms change.

That is why this topic matters for VINSCRIBE readers. It is not another title-brand story and it is not the same as negative equity. This is a deal-structure problem that shows up after the keys are already in your driveway. If you are not ready for it, the pressure can get expensive fast.

What yo-yo financing actually is

Yo-yo financing usually starts with spot delivery. The dealer lets you take the car home before outside financing is fully locked down. A day or two later, sometimes longer, they call and say the lender did not approve the deal on the original terms.

Step 1

Take the car home

The buyer leaves thinking the sale is done, even though financing approval may still be conditional.

Step 2

Get called back

The dealer says the lender would not buy the contract on the original rate or payment.

Step 3

Sign under pressure

Now the buyer is told to accept worse terms or unwind a deal that already feels finished.

The pressure point is simple. Once people have shown the car to family, moved insurance over, parked it at home, and mentally made it theirs, they become easier to push into a contract they would have rejected two days earlier.

Why this risk is different from the other used-car traps

Not a hidden-damage problem

The car itself might be fine. The trap is in the financing path, not just under the sheet metal.

Not the same as negative equity

Negative equity is balance math. Yo-yo financing is a contract-control problem that can raise the payment after you think the deal is done.

Not limited to bad-credit buyers

Buyers with decent credit can still get caught if they rely on dealer-arranged financing and do not pin down whether the approval is final.

The trade-in raises the stakes

Once your old car is mixed into the transaction, unwinding the deal gets more stressful and buyers lose leverage quickly.

That last point is what makes these deals messy. A buyer who arrived in one car and leaves in another is now negotiating from a much weaker spot than they were an hour earlier.

The warning signs before you drive off

-

The paperwork sounds conditional.

Watch for language that suggests the sale depends on later financing approval, assignment to a lender, or a later review by the finance office.

-

You are focused on monthly payment, not total terms.

That makes it easier for a dealer to come back later with a slightly higher payment and hope you will accept it to avoid starting over.

-

The dealer wants the trade-in immediately.

If your old vehicle is already being listed, moved, or detailed before financing is final, your exit gets harder.

-

You never see proof that the lender bought the contract.

If the answer to "Is financing fully approved and final right now?" gets slippery, slow down.

-

You are rushed into signing late in the day.

A lot of buyers miss conditional language when everyone in the room is trying to finish before closing.

If the dealer calls you back, do not walk in unprepared

This is the part where people start making expensive decisions just to make the discomfort stop. I would not go back to the dealership empty-handed or half-awake.

-

Ask what changed, in writing.

You want the specific reason the original contract was rejected and the full terms of the proposed replacement.

-

Compare APR, total financed amount, term length, and total of payments.

The monthly number alone can hide a much worse deal.

-

Confirm the status of your trade-in and down payment.

Do not assume those are easy to unwind once the original deal falls apart.

-

Bring your original signed paperwork.

You need the exact terms you already agreed to in front of you, not the dealership's version of your memory.

-

Be willing to walk.

If the only way the transaction survives is by getting materially worse, that is usually your answer.

The FTC's consumer advice on yo-yo financing is blunt for a reason: shop for financing before you shop for the car when possible, and if the dealer handles financing, ask whether the deal is final and get that in writing.

Where buyers lose the most money

APR shock

Higher cost over time

A few points of APR difference can turn a "close enough" decision into thousands of extra dollars.

Trade-in chaos

Less leverage

If your prior car is already gone or tied up, you are negotiating from a much weaker position.

Sunk-cost pressure

Bad terms accepted

Insurance changes, registration work, and emotional attachment make people accept deals they never wanted.

There is also a quieter cost here. Buyers who feel boxed in by financing pressure often stop scrutinizing the actual vehicle. That is exactly when title issues, prior damage, mileage inconsistencies, and open recalls stop getting the attention they deserve.

A safer used-car financing checklist

If I were buying a used car tomorrow and dealer financing was still on the table, this is the order I would use:

-

Get outside financing quotes first.

A bank or credit-union approval gives you a baseline and takes some of the theater out of the finance office.

-

Ask one direct question before signing: is the deal final right now?

Do not settle for a vague answer. If approval is conditional, treat the whole deal as conditional.

-

Read the contract for conditional-delivery language.

This is boring, but it is cheaper than finding out later that the paperwork gave the dealer room to rewrite the terms.

-

Keep your trade-in under your control until you understand the financing status.

Once your old car is absorbed into the deal, walking away gets complicated.

-

Run the VIN before you get emotionally trapped.

You want title, damage, theft, and recall context before you commit to the car and before the financing drama starts eating your focus.

Video briefings worth watching

These are actually useful for this topic because they show the contract-pressure part of the deal, not just generic "buy smart" advice.

Where VINSCRIBE fits into this

VINSCRIBE does not replace contract review or outside financing. It helps in a different part of the decision: keeping you from getting attached to the wrong car before the finance office starts trying to control the pace.

- Run the vehicle history before signing so you know whether the car deserves serious financing effort at all.

- Use the report to spot title, damage, theft, odometer, and recall signals that should change how aggressively you negotiate.

- Keep the vehicle facts separate from the dealership pressure. A shaky financing situation is the worst time to discover the car also has a shaky history.

That is the real value here. The more clarity you have before the emotional part of the purchase kicks in, the harder you are to push around later.